Why Is It SO Hard to Get Good Financial Advice? (+What To Do)

Why Is It SO Hard to Get Good Financial Advice? (+What To Do)

For many, getting good financial advice is difficult. Dave explains why and has two pieces of good news!

💈💈💈

Why are Canadians of normal-income means, of relatively modest wealth, struggling to get well-rounded, truly helpful financial advice? No, it’s not because all players in the financial industry are only out for themselves and greedy, greedy institutions and people. Well, some may be. No, it’s because providing advice to that group isn’t profitable for the most part.

For the advisor, it takes a lot of time and expertise. A great number of questions need to be asked. Then of course, a plan has to be formulated. Then specific recommendations have to be made. And on top of that, ongoing follow-up is important. If a client has, say, $20,000 in investable assets, maybe in a TFSA, the math just doesn’t work on the business-model front.

Perhaps they are saving for a home and they need to keep the money liquid in a savings account. Makes sense. But the advisor makes nothing. Hmm. Not a great trade-off for the hours it took to develop the plan. Or perhaps the client wants to purchase a mutual fund, but the advisor points out that it’s wiser instead to pay off their $20,000 credit card balance.

Solid advice. And put the client first. But earned zero commission. Or the young client doesn’t have any credit-card debt. Great. And it’s saving for the long term. Great. So the advisor intelligently puts the $20,000 in index funds. Again, zero commission. Nope, the advisor’s boss logically states, “This is dumb.

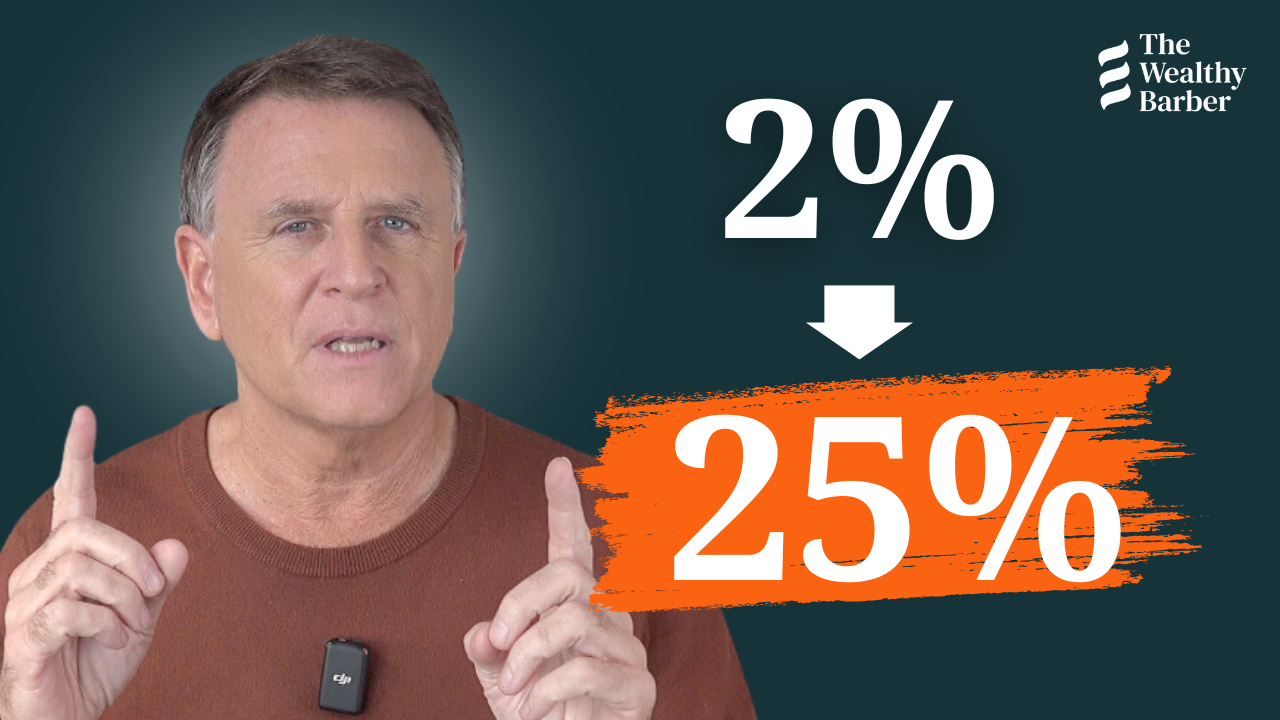

We need to make money. We’re not a charity. Put the $20,000 into a mutual fund with a high MER and we’ll at least get a 1% commission annually.” “Horrible,” you say. “They put their own interests first.” Fair, but kind of makes sense. Heck, even the 1% commission is only $200 that year. And remember, the advisor has to be paid for all those hours of creating the plan.

That’s only fair. Hmm, tough one. Giving advice to this group isn’t very lucrative and there are no economies of scale really. So, too often, the client ends up with the worst combination going – high-fee products AND a plan that, to be diplomatic, didn’t receive a lot of TLC, a lot of attention to detail. The follow-ups aren’t, well, following. So, what’s the answer? No easy response. But normal-income people often, of course, instead of being saddled with poor plans and lesser returns, should turn to learning more. They have to start doing more of this on their own, DIY. “Oh no, Dave! Don’t say that. I’m no good at this. I can’t grasp it.” You can. I promise.

It’s not that complicated. The tricky stuff doesn’t work. The simple products and approaches are almost always the best products and approaches. I can teach this stuff to you. And lots of other resources out there can help, too! We’ll point you towards many of them over the next few months. There are some great platforms now, by the way, that you can use – inexpensive and intuitive. And even more good news – planning technology is coming to save the day! It does scale. Marginal cost of zero. It’s inexpensive. It can now be customized and, with AI, even learn from you as it goes. I’ve seen two programs recently – wow, crazy impressive. You’ll have the Wealthy Barber, in essence, planning for you. A much smarter version, actually – right on your phone! Exciting. And maybe a little creepy, yeah.

Feel Confident About Your Finances

Sign up for our Weekly Round-Up of new videos and podcasts released over the past seven days. We won’t spam you or try to sell you a course—promise!